Filing an Income Tax Return (ITR) is often viewed as just another tedious administrative chore. For many whose income falls below the taxable threshold, the immediate thought is: “If I don’t owe any tax, why should I bother filing?”

However, filing your tax return is far more than just a legal compliance mechanism. It is a powerful financial tool that establishes your financial credibility and unlocks crucial economic opportunities. Whether your income is fully taxable or completely exempt, here is why keeping your tax record clean and updated is one of the smartest financial moves you can make.

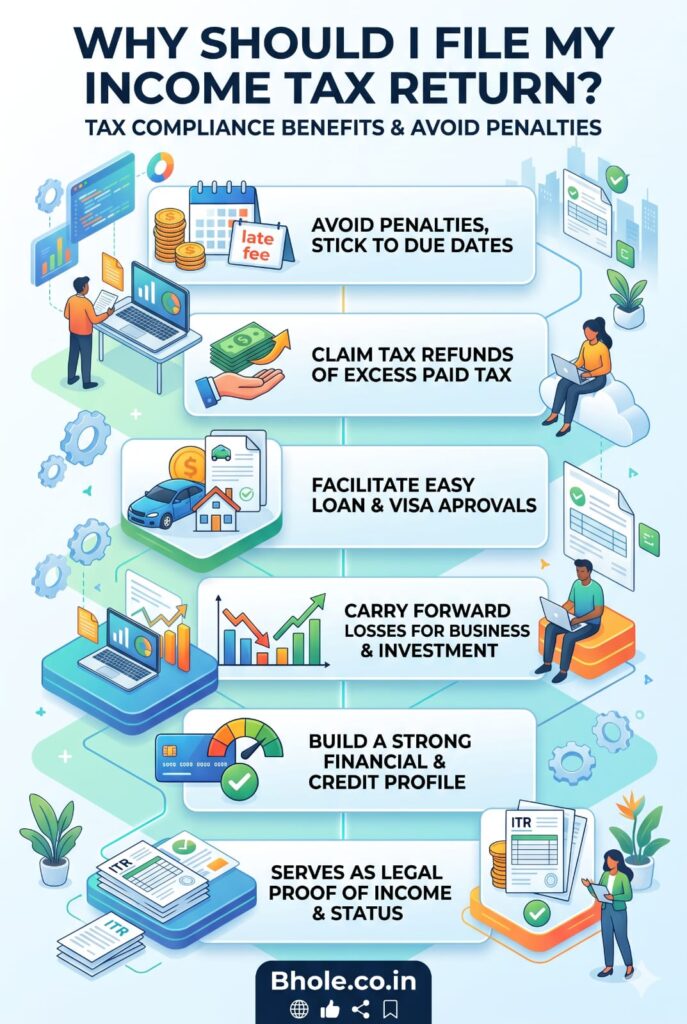

1.The Ultimate Proof of Financial Credibility

When you apply for a home loan, car loan, or business credit, banks do not just look at your current bank balance. They look for stable, documented income history.

Loan Approvals: Most major banks and financial institutions require the last 2 to 3 years of filed ITRs as mandatory documentation. It acts as the most authentic proof of your financial stability and repayment capacity.

Higher Credit Limits: Having a consistent track record of filing returns significantly boosts your trustworthiness, making it easier to secure higher credit card limits and favorable interest rates.

2.Fast-Track Your Global Travel (Visa Processing)

Planning to travel abroad for business, higher education, or a family vacation? Your visa application might rely heavily on your tax history.

Schengen, US, UK, and Canada Visas: Immigration authorities closely scrutinize an applicant’s financial ties to their home country to ensure they can support themselves.

The Trust Factor: A history of filed income tax returns serves as definitive proof that you are a tax-compliant citizen with a steady income source, drastically reducing the chances of a visa rejection.

3.Claiming Tax Refunds (Getting Your Money Back)

There are many instances where tax is deducted at source (TDS) on your earnings—such as interest on fixed deposits, professional fees, or contractual payments—even if your total annual income doesn’t fall into a taxable bracket.

The government cannot automatically refund this money to you.

The Only Way Out: The only mechanism to claim a refund of excess TDS deducted is by filing your income tax return. If you don’t file, that money stays with the government permanently.

4.Carry Forward Financial Losses

Life and business are full of market ups and downs. If you sustain capital losses from stock market trading, mutual funds, gold, or a business venture, you can use those losses to reduce your future tax liability.

The Catch: You can only carry forward these losses to offset against future gains if you file your tax return before the official due date.

Missing the due dates means losing the opportunity to shield your future profits from heavy taxation.

5.Avoiding Strict Penalties and Legal Notices

Tax laws are continuously evolving, and tax departments now use sophisticated data analytics to track high-value transactions—like buying property, investing heavily in mutual funds, or making large credit card payments.

If your financial footprint shows significant activity but your tax filing history is non-existent, it automatically triggers red flags.

Filing your return voluntarily ensures you stay compliant, avoiding hefty late fees, interest penalties, and unnecessary scrutiny from tax authorities.

The Takeaway: Filing your income tax return is an investment in your financial freedom. It builds your financial profile, keeps you legally secure, and ensures that you are ready to seize big opportunities—like buying a home or expanding a business—whenever they arrive. Don’t look at it as a burden; look at it as your financial passport.